A not so funny thing happened on the way to the release of our Financial State of the Cities. We used 2021 data, because most cities don’t have their 2022 data out yet. For 2021 there were crazy data swings. The most alarming was that San Francisco went from 67th worst city out of 75 to 2nd best. Los Angeles had a similar swing going from 44th worst to 4th best.

Of course, this led us to review the data more closely and what we found were huge amounts of reported investment income for the cities’ pension systems’ assets. For example, the San Francisco Employees’ Retirement System (SFERS) reported unrealized investment income of $9.4 billion, resulting in the system going from being $5.4 billion underfunded in 2020 to $2.6 billion overfunded in 2021. The system’s investments experienced unrealized gains of 35% for 2021. Unrealized means the system recorded the gains in their financial statements but they didn't actually receive cash because they didn’t sell the investments.

The Los Angeles Fire and Police Pension System (LAFPP) reported unrealized investment income of $7 billion for 2021 causing the system to go from being $2.6 billion underfunded to $2.7 billion overfunded. The 2021 system’s investments had unrealized gains of 32.56%. These huge rates of return, however, have been reversed for 2022.

While we couldn’t find 2022 data for SFERS, the LAFPP reported an unrealized investment loss of more than 7.23% in 2022, bringing the system back to an underfunded position of $649 million. We did find that both systems were among the 15 public pension systems that had assets in funds that had invested in FTX, the cryptocurrency trading company that has filed for bankruptcy. Founder, Sam Bankman-Fried resigned and is under indictment for at least eight criminal counts. The website for FTX is now inoperational and by most accounts, investors are unlikely to get any money back.

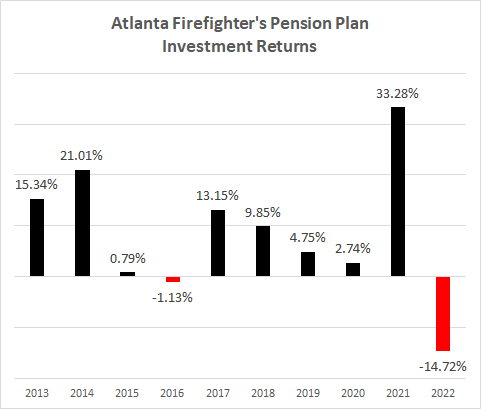

The Atlanta Firefighters’ Pension Plan (AFPP) experienced the biggest swing we could find, reporting an unrealized gain of 33.28% in 2021 and an unrealized loss of 14.72% in 2022. The chart below indicates the roller coaster ride AFPP investments have experienced in recent years. The 2021 to 2022 drop reminds me of the House of Terror ride.

The chart below includes the pension systems for which we found 2021 and 2022 investment net rates of return.

|

Plan Name |

Net Rate of Return |

|

|

FY 2021 |

FY 2022 |

|

|

Alaska PERS |

29.77% |

-6.00% |

|

Arizona Retirement Plans |

29.06% |

-4.37% |

|

Atlanta Firefighters’ Pension Plan |

33.28% |

-14.72% |

|

Atlanta General Employees’ Pension Plan |

31.35% |

-11.75% |

|

Atlanta Police Officers’ Pension Plan |

33.34% |

-13.45% |

|

CalPERS |

21.30% |

-6.10% |

|

Colorado PERA |

16.10% |

-13.70% |

|

Houston Firefighters' Fund |

33.40% |

-0.11% |

|

Houston Police Officers' Pension System |

32.30% |

-1.40% |

|

Indiana Public Employees' Retirement Fund |

25.50% |

-6.60% |

|

Los Angeles City Employees Retirement System |

27.50% |

-8.00% |

|

Los Angeles Fire & Police |

32.56% |

-7.23% |

|

Los Angeles Water & Power |

26.40% |

-5.39% |

|

Minnesota Correctional Fund |

30.21% |

-6.36% |

|

Minnesota General Employee Fund |

30.29% |

-6.23% |

|

Minnesota Police and Fire Fund |

30.27% |

-6.24% |

|

Minnesota Volunteer Firefighter Fund |

20.61% |

-13.08% |

|

New Mexico PERA Fund |

25.36% |

-3.11% |

|

Pennsylvania Public School Employees Retirement System |

24.57% |

2.40% |

|

Phoenix Employees' Retirement System |

22.80% |

-4.70% |

|

San Jose Federated City Employees' Retirement System |

29.43% |

-4.19% |

|

San Jose Police and Fire Pension Plan |

26.43% |

-4.81% |

|

Seattle Law Enforcement Officers and Fire Fighters' Retirement System |

31.00% |

1.00% |

|

Tennessee Teacher Pension Plans |

25.78% |

-3.83% |

|

Tucson Public Safety Personnel Retirement System |

27.76% |

-4.00% |

|

Virginia Retirement System |

27.50% |

0.60% |

Are these plans taking on riskier investments to meet their expected rates of return? The SFERS and the LAFPP use rates of return of 7.4% and 7%, respectively. We are currently looking at the pension systems’ asset allocations. As accountants, not investment managers, we don’t know what a reasonable asset allocation is. If you have thoughts on that, please let us know.

Maybe the most not-so-funny thing is that some people I talk to say they are grateful they don’t have investments in the stock market when it plummets, as it did in 2021. But, unfortunately, as taxpayers, you are in the market because your governments’ pension systems have stock market investments. If these investments go sour and the systems run out of assets before the promised benefits are paid, future taxpayers will most likely have to fund those benefits.